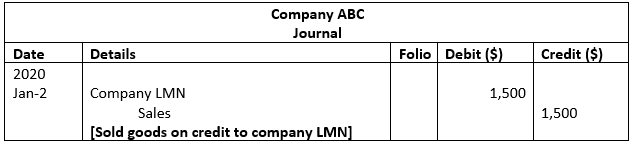

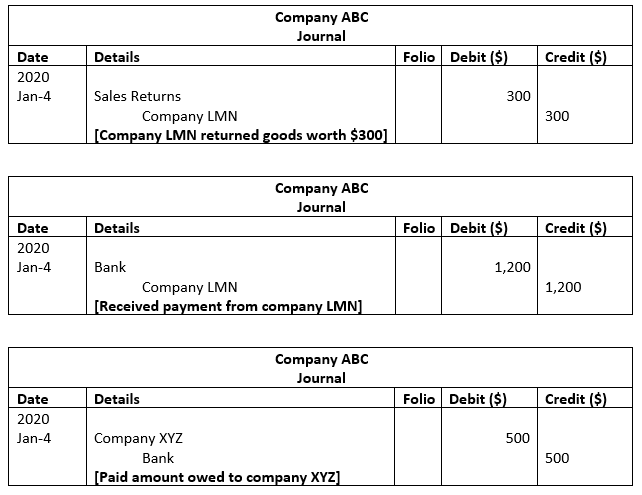

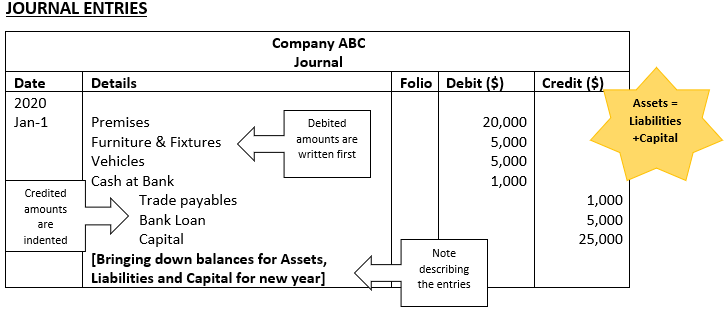

The Journal

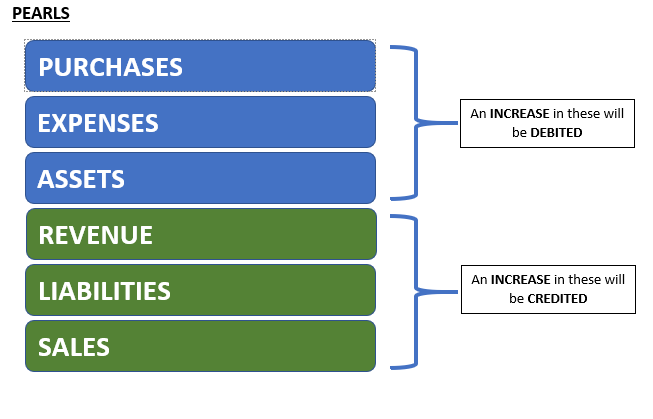

When a transaction, occurs, a business will first prepare a ledger before transferring the information to the ledger. The ledger shows the debit entries, credit entries and a short explanation about the transaction. To know what is debited and credited, you should know the three rules of accounting and PEARLS.

THE RULES OF ACCOUNTING

| Debited | Credited | |

| REAL ACCOUNTS (Assets) | What comes into the business | What goes out of the business |

| PERSONAL ACCOUNTS (All accounts associated with businesses/people) | The one who receives an amount/goods | The one who gives the amount/goods |

| NOMINAL ACCOUNTS (Expenses, Incomes, Losses and Profits) | All expenses and losses of a business | All sales and incomes of a business |

NOTE: The Folio column is used in a business to show the page number of the account being referenced. It will usually not be used during the examples, but it is still important to include when drawing the journal or the ledger.

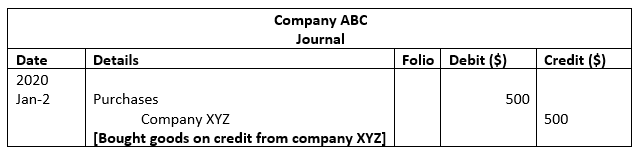

NOTE: Buying goods on credit means that you receive the goods from the company, but you do not pay them on that specific day. Selling goods on credit means you give goods to a company, but you do not receive payment from them on that particular day.