The price system and microeconomy

Price mechanism is allocation of resources in a market economy through the demand and supply of resources.

Key definitions of demand

Demand is the willingness and ability for a consumer to purchase a product at a different price per period time.

Notional demand is demand that is NOT backed up with the ability to purchase the product.

Effective demand is demand that is backed up with the ability to purchase the product.

The demand curve is represented by the relationship between the quantity demanded and the price of the product.

Demand schedule is the data from which a demand curve is drawn from.

Market demand is the total demand made by consumers in a market.

Demand

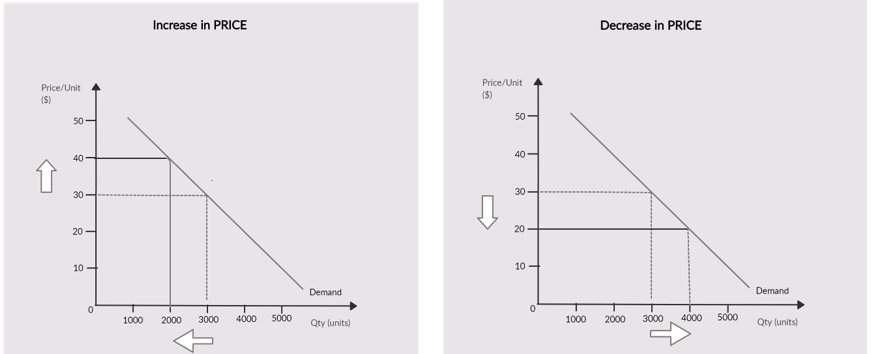

Demand and price have an inverse relationship.

For example: Price “↑” THEN demand “↓”

Price “↓” THEN demand “↑” Ceterus paribus in demand is when demand ONLY changes because of price

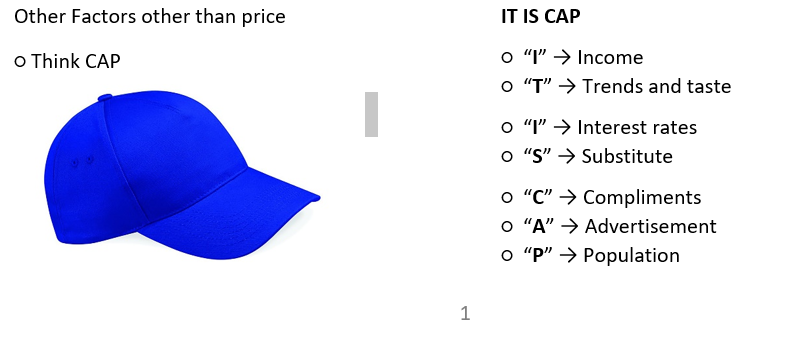

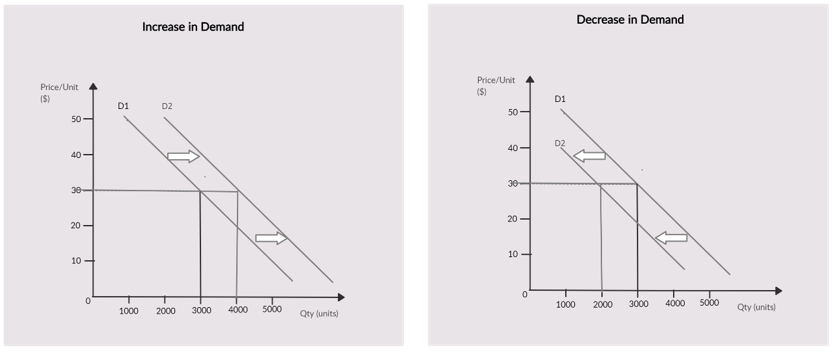

When other factors other than price affect demand, there is a shift in the demand curve.

Remember

Normal goods are goods that demands increase with an increase in income.

Inferior goods are goods that demand decrease with an increase in income.

Substitute goods are considered rival goods or alternative goods.

Complimentary goods are goods that are consumed with another, in order words, form a pair.

Joint demand is when two goods are consumed together. Occurs with complimentary goods.

Key definitions for supply

Supply is the willingness and ability for a producer to sell a product at a different price per period time.

Supply curve is represented by the relationship between quantity supplied and the price of a product.

Supply schedule is the data from which a supply curve is drawn from.

Supply

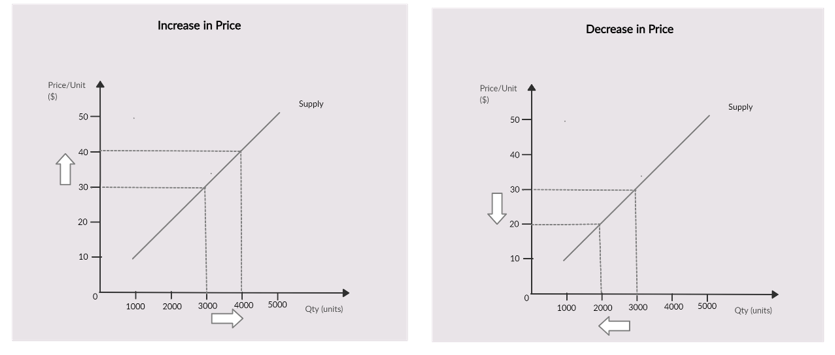

Supply and price have a direct relationship.

For example: Price “↑” THEN supply “↑”

Price “↓” THEN supply “↓” Ceterus paribus in supply is when supply ONLY changes because of price

Other Factors affecting supply, other than price:

○ Indirect Taxes

○ Subsidies

○ Climate

○ Lower cost of production

○ Technology

○ Competition

○ Productivity

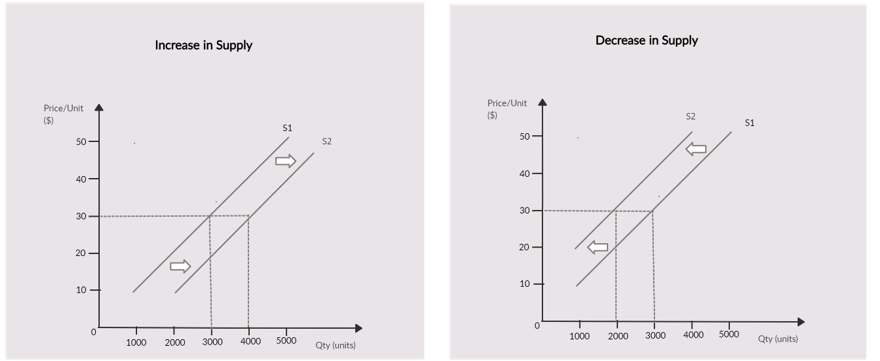

When other factors other than price affect supply, there is a shift in the supply curve.

Remember

Subsidies is a payment made by the government to producers to help them produce more or reduce market price. Note that it can be in the form of labour training or even financial aid.

Joint supply is when two items are produced together.

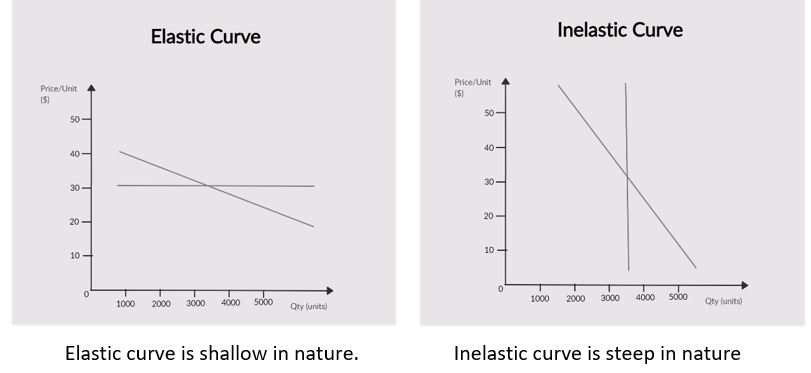

Price Elasticity of demand

○ Measures the responsiveness of quantity demanded with a change in price per period time.

○ The formula to find out the PED of a product is

○ IF PED : “>1”, then demand is price elastic.

“<1”, then demand is price inelastic.

“0”, then demand is perfectly price inelastic.

“∞”, then demand is perfectly price inelastic.

“1”, then demand is unitary price elastic.

○ PED is always negative because of the law of demand but we always imagine it as a positive integer

Determination of a good

A good can be determined if the demand is price elastic and inelastic based on some factors.

○ Number of substitutes for the product

○ If the product is addicting to consume

○ If the product is a luxury or a necessity

○ The time period → In the short run, demand is inelastic while in the long run, demand is elastic.

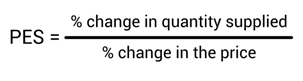

Price Elasticity of supply

○ Measures the responsive of quantity supplied with a change in price per period time

○ The formula to find out the PES of a product is

○ IF PES : “>1”, then supply is price elastic.

“<1”, then supply is price inelastic.

“0”, then supply is perfectly price inelastic.

“∞”, then supply is perfectly price inelastic.

“1”, then supply is unitary price elastic.

○ PES is always positive because of the law of supply

Determination of a good

A good can be determined if the supply is price elastic and inelastic based on some factors.

○ Stock size → larger stock meaning elastic and smaller stock meaning inelastic. In the case of a hotel

or cinema, the number of seats available are limited. Therefore inelastic

○ Spare productive capacity → high then elastic and if spare capacity is low then inelastic. In the case

of agriculture, it takes time to change the types of crops.

○ Time period → In the short run, supply is inelastic while in the long run, supply is elastic as it

cannot vary the factors of production in the short run.

Elasticity and inelasticity

Elasticity is when the change in demand/supply is greater than the change in price. Inelasticity is when the change in demand/supply is less than the change in price

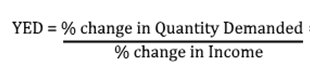

Income elasticity of demand

○ Measures the responsiveness of the quantity demanded with a change in income per period time.

○ The formula to find out YED of a product is.

○ IF YED : “>1”, then demand is income elastic.

“<1”, then demand is income inelastic.

“0”, then demand is perfectly income inelastic.

“∞”, then demand is perfectly income inelastic.

“1”, then demand is unitary income elastic.

○ YED can be both positive and negative. Positive meaning normal good and negative meaning inferior good.

○ If YED is positive and elastic, that means it is a normal luxury good, and if YED is positive and inelastic, that means it is a normal necessity good.

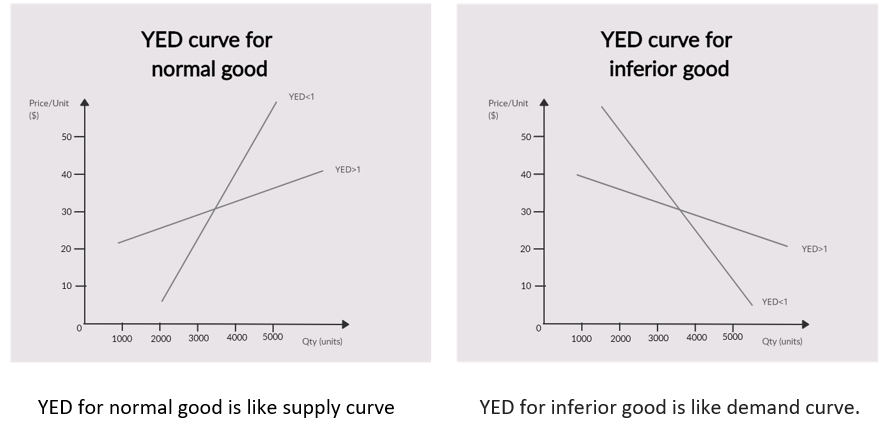

Cross elasticity of demand

○ Measures the responsiveness of quantity demanded of a good/service with a change in price of another good/service

○ The formula to find out XED of a product is.

○ IF XED : “>1”, then demand between the two goods/service is elastic (strongly related)

“<1”, then demand between the two goods/services is inelastic (weakly related)

“0”, then demand between the two goods/services is perfectly price inelastic (no relation)

○ XED can also be both positive and negative. Positive meaning substitutes good and negative meaning complimentary good.

Equilibrium is a situation where demand and supply are equal and is the point where the demand curve intersects with the supply curve.

Disequilibrium is a situation where demand and supply are not equal.

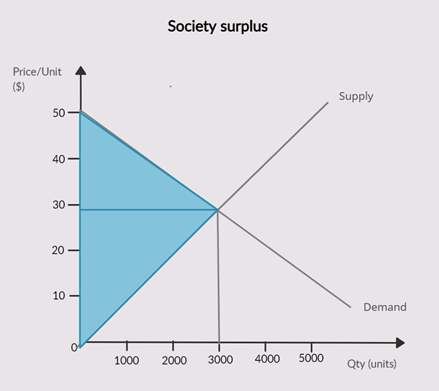

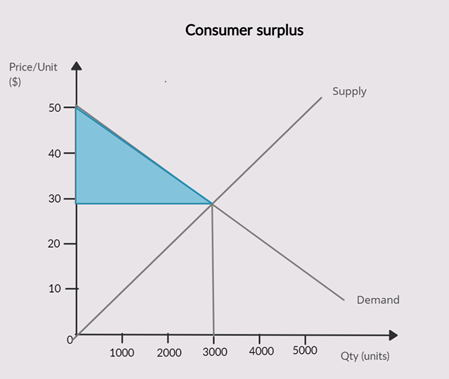

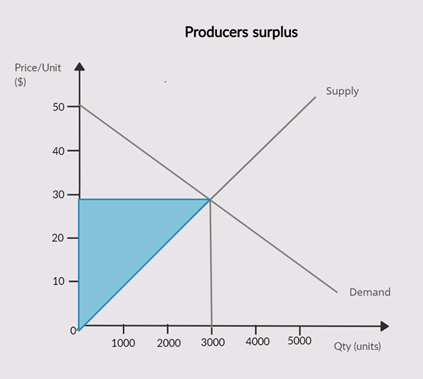

Consumer and producer surplus

Consumer surplus

○ Consumer surplus is the difference between the price that consumers are willing and able to pay

for a good/service, compared with the price they pay.

○ It is situated below the demand curve and above the price line

Producer surplus

○ Producer surplus is the difference between the price producers are willing and able to sell for a

good/service compared with the price they receive.

○ It is situated above the supply curve and below the price line

Society Surplus

○ Society surplus is simply the consumer surplus + producer surplus

○ You can imagine that the society surplus takes up both the regions