Basic economic ideas and resource allocation

Economic efficiency:

Where scarce resources areused in the most efficient way to produce maximum output.

Economic efficiency consists of:

- Productive efficiency: This occurs when firms produce at the lowest possible cost. A firm is productively efficient when it makes the best use of resources and producing at the lowest possible cost

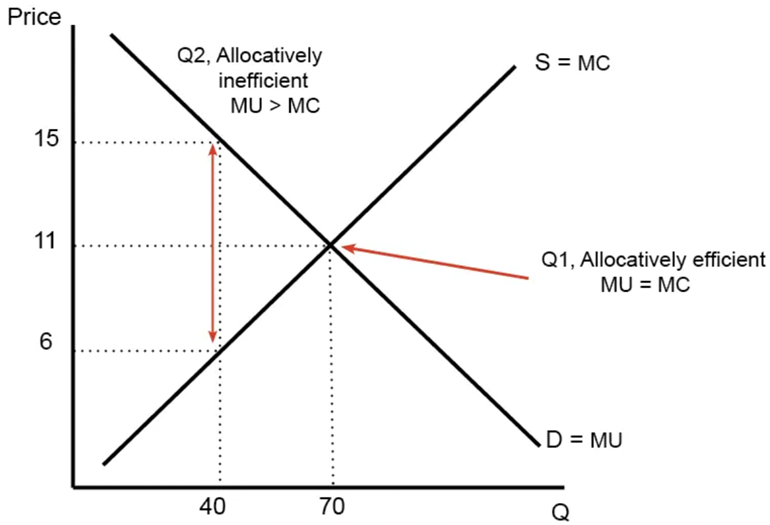

- Allocative efficiency: This occurs when firms produce the combination of goods and services that are most wanted by the consumers

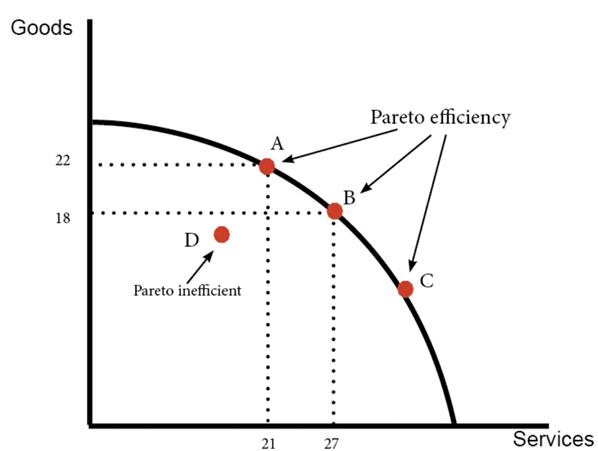

- Pareto optimality: Where it is impossible to make someone better off without making someone else worse off

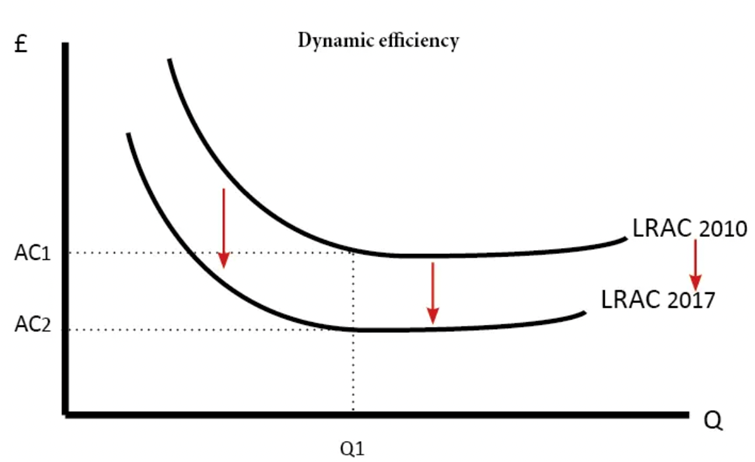

- Dynamic efficiency: It is a form of productive efficiency that benefits a firm over time

Market Failure:

There are various reasons why market failure occurs. They include:

- where there are externalities present in the market

- the provision of merit and demerit goods

- the provision of public and quasi-public goods

- Information failure

- adverse selection or moral hazard

- abuse of monopoly power in the market

Externality: Where the actions of producersor consumers give rise to side effects on third parties who are not involved in the action

It is further possible to distinguish when the externalities are the result of production or consumption decisions. Typical examples are:

Negative production externalities: These are spillover effects that occur as a result of production activity. A common case is that of most forms of environmental pollution.

Negative consumption externalities: These are created by consumers as a consequence of their use of products that result in harm to others who are not involved in the consumption. A very relevant and topical global example is that of passive smoking

Positive production externalities: These are benefits to third parties and are created by producers of goods and services. A typical example is when, as a result of medical research, a new drug or vaccine is developed to combat a serious disease.

Positive consumption externalities: Here, the benefits are the spillover effects of consumption of a good or service on others.

Externalities and Inefficient resource allocation

Socialcosts: the totalcosts of a particular action. Privatecosts: those costs that are incurred by an individual who produces a good or service.

External costs: those costs incurred and paid for by third parties not involved in the action.

Social benefits: the total benefits arising from a particular action.

Private benefits: benefits that accrue to individuals who produce or consume a particular good.

External benefits: benefits that that are received by third parties not involved in the action.

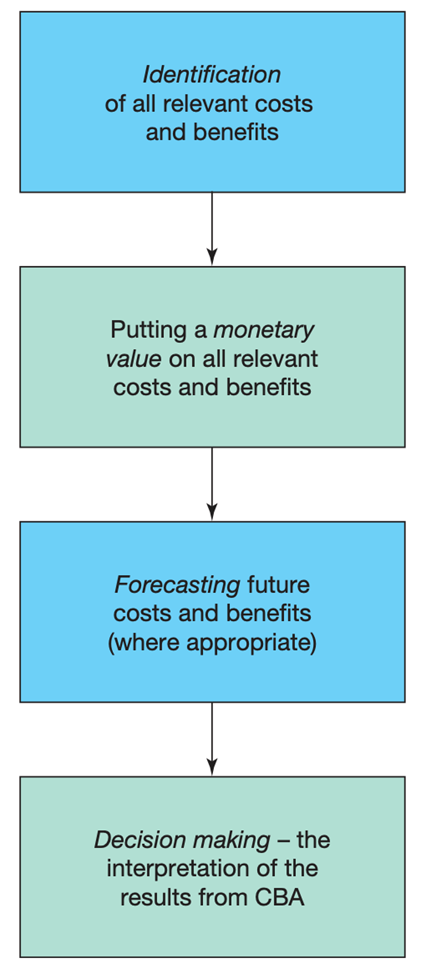

Cost benefit analysis in Decision making

Cost–benefit analysis (CBA): a method for assessing the desirability of a project taking into account the costs and benefits involved.

Shadowprice: one that is applied where there is no recognised market price available.