The Marketing Mix – PRODUCT AND PRICE

MARKETING MIX

- The four key decisions that must be taken in the effective marketing of a product

- Product- this might be an existing product, an adaptation of an existing product or a newly developed one.

- Price- if the price is set too low, then consumers might lose confidence in the product’s quality; if too high, then many will be unable or unwilling to

afford it. - Promotion- telling consumers about the product’s availability and convincing them, if possible, that your brand is the one to choose.

- Place- how the product is distributed to the consumer; if it is not available at the right time in the right place, then even the best product in the world will not be bought in the quantities expected

THE ROLE OF THE CUSTOMER- THE 4 Cs

- The 4 Cs is an alternative view of the key elements of successful marketing

- Customer solution – what the firm needs to provide to meet the customer’s needs and wants.

- Cost to customer – the total cost of the product including extended guarantees, delivery charges and financing costs.

- Communication with customer – providing up-to-date and easily accessible two-way communication links with customers to both promote the product and gain back important consumer market research information.

- Convenience to customer – providing easily accessible pre-sales information and demonstrations and convenient locations for buying the product.

- Customer Relationship Management (CRM)- using marketing activities to establish successful customer relationships so that existing customer loyalty can be maintained.

- 4Ps and 4Cs relation-

- Product – Customer solution

- Price – Cost to customer

- Promotion – Communication with customer

- Place – Convenience to customer

- How to improve customer relations-

- Targeted marketing

- Customer service and support

- Providing as much information to customers as possible

- Using social media

PRODUCT

- Product- the end result of the production process sold on the market to satisfy a customer need

- The term ‘product’ involves consumer and industrial goods and services

- Goods have a physical existence such as laptops, candy, microwaves, etc.

- Services have no physical existence but satisfy consumer needs in other ways such as car repairs, banking, hair styling, etc.

- Unique Selling Point (USP)- the best form of product differentiation is one that creates a USP

- Benefits of an effective USP-

- Effective promotion that focuses on the differentiating feature of the product or service.

- Opportunities to charge higher prices due to exclusive design/service.

- Free publicity from business media reporting on the USP.

- Higher sales than undifferentiated products.

- Customers more willing to be identified with the brand because ‘it’s different’.

- Benefits of an effective USP-

- Tangible attributes of a product- measurable features of a product that can be compared to that of another product

- Intangible attributes of a product- subjective opinions of customers about a product that cannot be measured or compared easily

- Brand- an identifying symbol, name, image, or trademark that distinguishes a product from its competitors

- Product positioning- the consumer perception of a product or a service compared to its competitors

- Before deciding on which product to develop and launch, it is common for firms to analyze how the new brand will relate to the other brands in the market, in the minds of consumers.

- The first stage is to identify the features of this type of product considered to be important to consumers – as established by market research. These key features might be price, quality of materials used, perceived image, etc. They will be different for each product category.

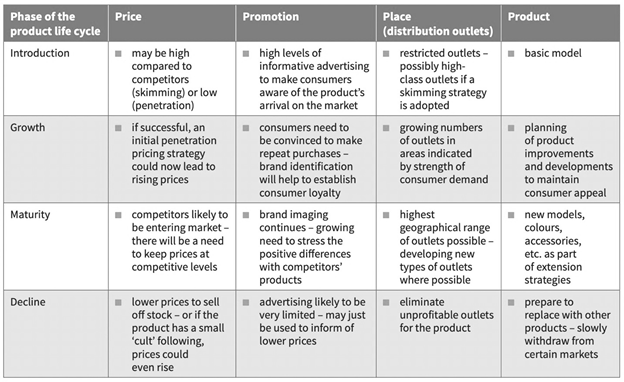

- Product Life Cycle- the pattern of sales recorded by a product from launch to withdrawal from the market and is one of the main forms of product portfolio analysis

- Introduction stage- this is when the product has just been launched after development and testing; sales are often quite low to begin with and may increase only quite slowly

- Growth stage- if the product is effectively promoted and well received by the market, then sales should grow significantly

- Maturity/saturation stage- sales fail to grow but they do not significantly decline either

- Decline stage- sales will decline steadily; either no extension strategy has been tried or it has not worked, or the product is so obsolete that the only option is a replacement

- Extension strategies- these strategies aim to lengthen the life of an existing product before the market demands a completely new product

- Examples- selling in new markets, repackaging and relaunching the product, finding new uses for the product

- Extension strategies- these strategies aim to lengthen the life of an existing product before the market demands a completely new product

- Uses of the product life cycle

- Assisting with planning marketing mix decisions such as new product launches or promotions changes

- Identifying how cash flow might depend on the cycle

- Recognizing the need for a balanced product portfolio

- Identifying how cash flow might depend on the product life cycle

- Development- cash flow is negative during the development of the product as costs are high, but nothing has yet been produced or sold.

- Introduction- the development costs might have ended but heavy promotional expenses are likely to beincurred – and these could continue into the growth phase. In addition, there is likely to be much unused factory capacity at this stage, which will place a further strain on costs. As sales increase, then cash flow should improve – precisely when this will happen will depend on the length of consumer credit being offered.

- Maturity- most positive cash flows, because sales are high, promotion costs might be limited, and spare factory capacity should be low.

- Decline- price reductions and falling sales are likely to combine to reduce cash flows. Clearly, if a business had too many of its products either at the decline or the introduction phase, then the consequences for cash flow could be serious

- Identifying the need for a balanced product portfolio

- As one product declines, so other products are being developed and introduced to take its place.

- Cash flow should be reasonably balanced, so there are products at every stage and the positive cash flows of the successful ones can be used to finance the cash deficits of others.

- Factory capacity should be kept at roughly constant levels as declining output of some goods is replaced by increasing demand for the recently introduced products

- Evaluation for product life cycle

- This is an important tool for assessing the performance of the firm’s current product range. It is an important part of a marketing audit – a regular check on the performance of a firm’s marketing strategy.

- However, the product life cycle is based on past or current data and it cannot be used to predict the future. Just because a product’s sales have grown over the past few months does not mean that they will continue to grow until a long period of maturity is reached – sales could crash very quickly with no chance of an extension strategy being employed.

- To be really useful, a product life-cycle analysis needs to be used together with sales forecasts and management experience to assist with effective product planning.

- Evaluation for product portfolio analysis

- Managing product portfolios effectively can help a business achieve its marketing objectives. Products cannot just be ‘launched and forgotten’ but must

be developed, marketed and managed to help the business increase sales profitably. - The product is often considered to be the most important element of the marketing mix, because if it fails to work, is poorly designed and looks ugly, low prices and extensive advertising may not help much.

- However, product is just one part of the overall strategy needed to win and keep customers. Price, promotion and place are also key factors in making products successful – and a balanced and integrated marketing mix is essential. But without a well managed product portfolio that offers customer real and distinctive benefits, marketing objectives are unlikely ever to be achieved.

- Managing product portfolios effectively can help a business achieve its marketing objectives. Products cannot just be ‘launched and forgotten’ but must

PRICE

- Price is the amount paid by customers for a product

- The pricing level set for a product will also-

- determine the degree of value added by the business to bought-in components

- influence the revenue and profit made by a business due to the impact on demand

- reflect on the marketing objectives of the business and help establish the psychological image and identity of a product.

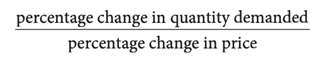

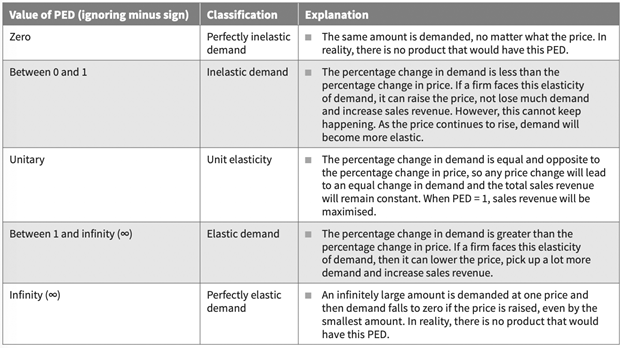

- Price elasticity of demand- measures the responsiveness of demand following a change in price

- Factors that determine price elasticity

- Necessity of the product- the more necessary a product is, the less they will react to price changes; this makes demand more inelastic

- Availability of substitutes- if there are many substitutes of a product, consumers can quickly switch to another brand if the price of one manufacturer’s product increases

- Level of consumer loyalty- if a firm has a high degree of customer loyalty, then their consumers will be likely to continue purchasing from them following a rise in price

- Price of the product as a proportion of consumers’ incomes- a cheap product that takes up a small proportion of consumers’ incomes is likely to have inelastic demand

- Applications of price elasticity of demand

- Making more accurate sales forecasts- if a business is considering a price increase, perhaps to cover rises in production costs, then an awareness of PED should allow forecast demand to be calculated.

- Assisting in pricing decisions- for example, if an operator of bus services is considering changing its pricing structure, then, if it is aware of the PED of different routes, it could raise prices on routes with low PED (inelastic) and lower them on routes with high PED

- Evaluation of PED

- PED assumes that nothing else has changed. If Firm A reduces the price for a product by 10%, it will expect sales to rise because of this – but if, at about the same time, a competitor leaves the industry and consumer incomes rise, the resulting increase in sales of Firm A’s product may be very substantial, but not solely caused by the fall in price. Calculating PED accurately in these and similar situations will be almost impossible.

- A PED calculation, even when calculated when nothing but price changes, will become outdated quickly and may need to be often recalculated because over time consumer tastes change and new competitors may bring in new products – so last year’s PED calculation may be very different to one calculated today if market conditions have changed.

- It is not always easy or possible to calculate PED. The data needed for working it out might come from past sales results following previous price changes. These data could be quite old and market conditions might have changed. In the case of new products, market research will have to be relied upon to estimate PED – by trying to identify the quantities that a sample of potential customers would purchase at different prices. This will be subject to the same kind of inaccuracy as other forms of market research.

- How is price determined?

- Costs of production- the price of a product must cover all the costs of producing it and of bringing it into the market; these costs include the variable costs and the fixed costs

- Competitive conditions in the market- if the firm is a monopolist, it is likely to have more freedom in price setting than if it is one of many firms making the same type of product; similarly, a firm with a high market share is likely to be a price setter that sets prices for other smaller firms to follow

- Competitor’s prices- the more competition the more likely it is that the prices will be fixed similar to those fixed by other businesses

- Business and marketing objectives- if the aim is to become a market leader through mass marketing, then this will require a different price level compared to a business that targets a niche market

- Price elasticity of demand

- Whether the product is new or already existing- new products may choose to adopt either a skimming or penetration strategy

- Pricing methods

- Cost-based pricing

- Firms will assess their costs of producing or supplying each unit, then add an amount on top of the calculated cost

- Mark-up pricing- adding a fixed mark -up for profit to the unit price of a product

- Target pricing- setting a price that will give a required rate of return at a certain level of output/sales

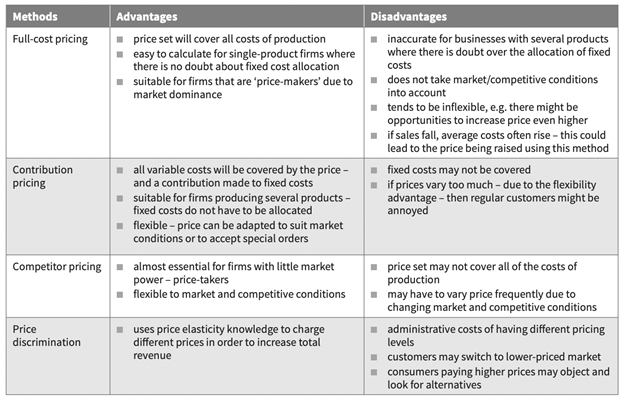

- Full-cost pricing- setting a price by calculating a unit cost for the product (allocated fixed and variable costs) and then adding a fixed profit margin

- Contribution-cost pricing- setting prices based on the variable costs of making a product in order to make a contribution towards fixed costs and profit

- Competition based pricing- a firm will base its price upon the price set by its competitors

- Price discrimination- charges customers different prices for the same product or service based on what the seller thinks they can get the customer to agree to

- Cost-based pricing

- Pricing strategies for new products

- Penetration pricing- setting a relatively low price often supported by strong promotion in order to achieve a high volume of sales

- Market skimming- setting a high price for a new product when a firm has a unique or highly differentiated product with low PED

- Issues with pricing decisions

- Level of competition

- Price wars to gain market share- these can be very damaging to profits and can even lead to weaker firms being forced out of the industry; this might reduce long-term competition which could eventually lead to higher prices and reduce the pressure on firms to innovate

- Non-price competition- competition through promotional campaigns that are designed to establish brand identity and dominance

- Collusion- involves people or companies which would typically compete against one another, but who conspire to work together to gain an unfair market advantage

- Loss leaders- commonly used by retailers; it involves the setting of very low prices for some products in the expectation that consumers will buy other goods too- the firms hope that the profits earned by these other goods will exceed the loss made on the low-priced ones

- Psychological pricing- it is very common for manufacturers and retailers to set prices just below the price levels in order to make the price appear much lower than it is; it also refers to the use of market research to avoid setting prices consumers consider to be inappropriate for the style and quality of the product

- Level of competition

- Evaluation of pricing decisions

- It would be incorrect to assume that one firm will use the same pricing method for all of its products- market conditions for the different products could vary greatly therefore, it would be important for the business to apply different methods to its portfolio of products, depending on costs of production and competitive conditions within the market.

- Level of price can have such a powerful influence on consumer purchasing behaviour that marketing managers should ensure that market research is used to test the impact of different levels of price on potential demand.

- In the world of FMCGs, there is often little to be gained by adopting a low-price strategy at all times – consumers expect good value, not necessarily low prices. ‘Good value’ means that all aspects of the marketing mix are combined and integrated together so that consumers accept the overall position of the product and agree that its image justifies the price charged for it.

- In assessing whether a product offers good value, price is only one factor. The complete brand image or lifestyle offered by the good is increasingly important in a world where many consumers have so much choice and their incomes are rising.

- Pricing strategies for new products

- Penetration pricing- setting a relatively low price often supported by strong promotion in order to achieve a high volume of sales

- Market skimming- setting a high price for a new product when a firm has a unique or highly differentiated product with low PED

- Issues with pricing decisions

- Level of competition

- Price wars to gain market share- these can be very damaging to profits and can even lead to weaker firms being forced out of the industry; this might reduce long-term competition which could eventually lead to higher prices and reduce the pressure on firms to innovate

- Non-price competition- competition through promotional campaigns that are designed to establish brand identity and dominance

- Collusion- involves people or companies which would typically compete against one another, but who conspire to work together to gain an unfair market advantage

- Loss leaders- commonly used by retailers; it involves the setting of very low prices for some products in the expectation that consumers will buy other goods too- the firms hope that the profits earned by these other goods will exceed the loss made on the low-priced ones

- Psychological pricing- it is very common for manufacturers and retailers to set prices just below the price levels in order to make the price appear much lower than it is; it also refers to the use of market research to avoid setting prices consumers consider to be inappropriate for the style and quality of the product

- Level of competition

- Evaluation of pricing decisions

- It would be incorrect to assume that one firm will use the same pricing method for all of its products- market conditions for the different products could vary greatly therefore, it would be important for the business to apply different methods to its portfolio of products, depending on costs of production and competitive conditions within the market.

- The level of price can have such a powerful influence on consumer purchasing behavior that marketing managers should ensure that market research is used to test the impact of different levels of price on potential demand.

- In the world of FMCGs, there is often little to be gained by adopting a low-price strategy at all times – consumers expect good value, not necessarily low prices. ‘Good value’ means that all aspects of the marketing mix are combined and integrated together so that consumers accept the overall position of the product and agree that its image justifies the price charged for it.

- In assessing whether a product offers good value, price is only one factor. The complete brand image or lifestyle offered by the good is increasingly important in a world where many consumers have so much choice and their incomes are rising.